- >>

- LIFE

Insurance Workers Say Things Are Murky on the Ground

Cutthroat competition, lean demand

Covid lockdowns in the last two years have really hit the economy very hard, sparing almost none of the sectors. Like the other sectors, the lockdowns have taken a toll on the insurance business as well. But what is happening on the ground in this sector is something very murky, and should be of great concern to the authorities.

Although The Citizen mainly spoke with insurance functionaries in Himachal Pradesh, the scenario according to them is pretty similar in several other states.

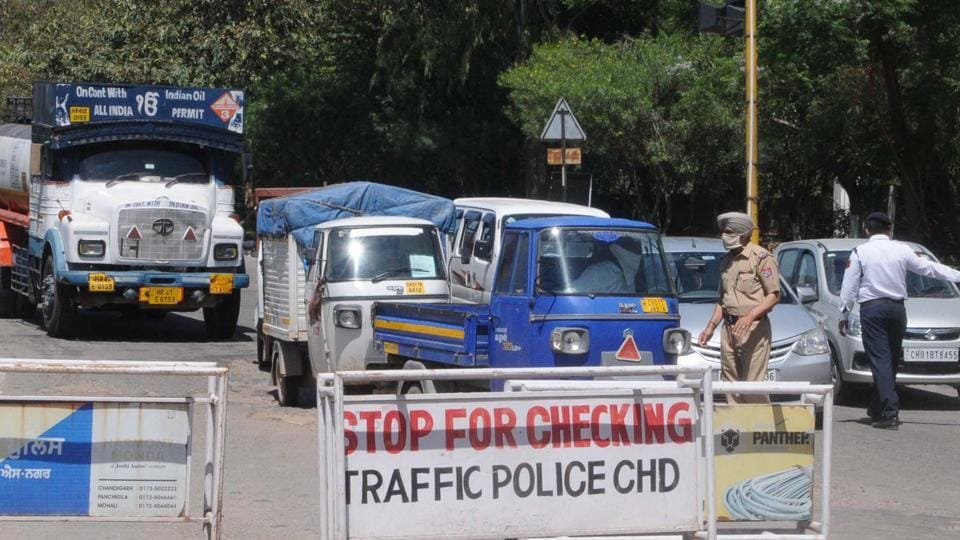

One of the surprising facts they disclosed pertains to mandatory vehicle insurance. They said that a fairly large number of owners with vehicles for both personal and commercial use are not getting their insurance renewed. The reason is the ever increasing premium costs, and earnings having dipped considerably because most commercial vehicles haven’t been plying during the lockdowns.

So what are they resorting to? Firstly, if a person owns five vehicles for commercial use, they are getting the insurance renewal for only two, letting the other three remain idle since the volume of work continues to be low.

“I have three cranes for towing away vehicles that get stuck in the hills from an accident or breakdown. Right now I am just operating just one of them as I cannot afford to pay premiums for the other two,” said Sunil Kumar, who tows vehicles stuck in parts of Sirmaur, Solan, Shimla and Kinnaur.

“There was hardly any work during the lockdown. The insurance premium for the one I am operating too was paid by one of my customers who was not in an position to pay the amount I had quoted for service and promised to pay my premium instead,” he said.

“The case is the same with truck owners affiliated to big unions like the one at Darlaghat. A large number of them are delaying paying insurance premiums as their vehicles have remained idle for long,” shared a politician from the area.

Abhishek Mithoo, who provides insurance services of all sorts in Solan, pointed to another disturbing trend in vehicle insurance. “People have been resorting to frauds. Many times they take out cover notes of old policies, edit the dates and take fresh printouts while plying their vehicles for personal use.

“In other cases, they get a policy made and pay through a cheque which bounces. Even as their insurance policy gets forfeited immediately in the company records, they continue moving around with the document obtained while making the payment through cheque for one year.”

At the local level many people are moving about without getting their insurance renewed. In certain cases the cops too have been taking a lenient view knowing that people who have barely been able to purchase two-wheelers are hard pressed for paying the annual premiums.

Insurance professionals have been hit badly from all sides. They point out that economic compulsions have compelled people to take third-party insurance for their personal vehicles instead of comprehensive plans that cover the vehicle in case of damage as well as the victim in case of an accident.

Then there is the cutthroat competition among private insurance companies offering different rates, and above all the entry of a very large number of agents who are partially trained and often resort to wrong selling of the products available.

They say that when it comes to actually claiming insurance, most people do not know how to go about things. The same is the case with semi-trained agents who are often jumping around from one company to another. They sell a policy of one company to a person and when the latter approaches them for claims they are found to have changed their company. This is leading to a lack of trust among customers in small towns.

“Another thing to be factored here is the entry of a whole lot of NBFCs (non-banking financial companies) getting their staff to sell insurance plans against high targets. This is because their original tasks of financing houses and other things are yet to pick up because of the economic downturn,” said Mithoo.

“There doesn’t seem to be any solution in sight unless things are addressed at the policy level. The competition is such that it has resulted in such a mess,” said Arun, who heads a local branch of one of the insurance companies.

Many insurance professionals say that their business has come down to just 20% of what it used to be a couple of years ago.

“One of the solutions to the present mess can be reduction in the annual premiums of commercial vehicles, so that everyone comes forward for renewals on due dates. The second can be making comprehensive policies compulsory for certain set of vehicles,” said Karam, who heads a branch of another company.

Things are pretty confusing even in the health insurance sector, where too a lot of wrong selling is being done. Very few customers are aware of the products being sold to them by glib talkers. They do not understand what is covered and what is not under the policy that they purchase. Here too there is very little consistency of agents sticking to one company.

At present there are 57 insurance companies, both government and private operating in India. Of these 33 are into sectors other than life insurance. Professionals in the sector believe that the regulatory authorities need to step in to put the sector on the right track by checking the lacunas on the ground.