- >>

- WORLD

LONDON: Chaos is a Greek concept. According to Greek mythology, chaos was the origin of everything. It was the primordial void, the source out of which everything was created, including the universe and the gods. Today, in Greece, chaos means something entirely different -- but has come to be equated with the cash-strapped country’s economy.

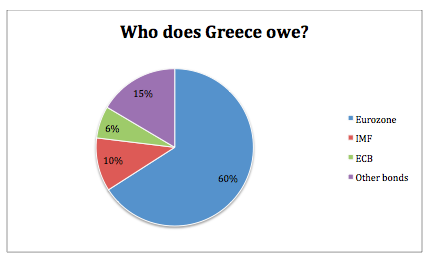

Greece, to put it mildly, is in trouble. The immediate cause of trouble is the fact that the country needs to secure funds from its creditors to make a $1.8bn payment to the International Monetary Fund. The larger trouble is the to270bn that the country owes. The chart below explains how much it owes to whom.

Now the most pertinent question to ask is: how did Greece land itself in so much trouble? The standard account that you will find in most articles in the mainstream media will lead you to believe that Greece signed up for this mess. The country was wrecked by the financial crisis in 2008 (this part, for the record, is true) and borrowed more money than it has been able to generate. To pay back its loans in installments, it has borrowed more money -- thereby trapping itself in a financial mess. The present trouble stems from the fact that Greece seems to have had enough. A left-wing government that was elected to power based on its opposition to austerity measures -- which, in turn was imposed on Greece by its creditors -- is in the process of negotiating the bailout terms to secure funds to pay off the IMF loan that was due on Tuesday this week. The creditors have refused to extend the bailout, and the whole European economy -- and the European Union itself -- is in jeopardy.

Now here is what is wrong with the above all-too-familiar narrative. Firstly, the loans that were made to Greece in 2010 and 2011 were not made by public institutions such as the ECB and IMF (who Greece now owes the money to). They were made to Greek firms mainly by German and French banks in pursuit of high profits. Soon after, these banks realized that the loans were a risky proposition. The banks were then bailed out (Greece was not bailed out) by transferring the debt from the banks to institutions likes the ECB and IMF. Now, the ECB and IMF dictate the terms of Greece’s repayment -- and are are trying to force the Greek government to cut pensions, education, salaries, and health care to pay for the bail out of the banks.

Secondly, it is interesting to note that the German nation owes as much money to the Greek people as Greece owes to Germany and the ECB combined. However, Greece cannot collect this money because Germany has the political and economic power (and allies such as the US) to enforce debt repayment.

Unfortunately, there is truth now in the statement that Greece is in a deep mess. It has every right to oppose the austerity measures (and the Greek people who are directly impacted by these cuts made their displeasure felt by voting in the anti-austerity Syriza party). The austerity measures have forced upon Greece another recession austerity policies have produced a decline in the Greek economy by over 25% since 2010.

An article by Duane Campbell (professor emeritus at California State University Sacramento) -- which for the record is a major source of information for this article -- states, “here are significant and complex economic issues here, but it is equally important to not allow narrow, technocratic, bankers' and economists' insiders views to go unchallenged. The problem is not that they are technocrats, but that their numeracy (number crunching) disguises a particular set of political assumptions that enriches and protects the wealthy at the expense of everyone else.

The domination of discussion in the media and in academia by a narrow and limited view of economics allows the neoliberal (pro- finance capital) assumptions to determine policy. To understand this process of wealth extraction, we need to recognize how debt has been transferred from banks to nominally "public" institutions such as the IMF and the European Central Bank.

The bankers' assumptions produce policy choices that make the rich richer and the poor poorer. They are not the product of a science of economics but of the well-financed pursuit of self interest and the promotion of profit by the financial oligarchy. To begin to comprehend an alternative, you need to understand, along with Greek Finance Minister Yanis Varoufakes, that this is not a Greek crisis, it is a Eurozone crisis that is currently having its most devastating effects on the people of Greece, Spain, Portugal and Italy, and immigrant minorities in France, among others.”

You can watch the explanation here:

You can’t blame the Greek people for being angry about the very same austerity measures that have pushed it into a deep, deep recession. The austerity demands of European bankers and politicians have shattered the Greek economy, with layoffs, wage and pensions reductions and huge cutbacks in healthcare pushing almost 44 percent of the Greek people below the poverty line.

A major sticking point on the funds for the repayment to the IMF is the slashing of retirement pensions. Greece is refusing to slash retirement pensions, and the creditors are insisting that it does.

Retirement pensions in Greece have already been slashed massively. Since 2010, main pensions have been slashed 44 to 48 percent -- reducing the average pension to 700 euros a month . About 45 percent of Greek pensioners receive less than 665 euros monthly -- a figure below the official poverty threshold.

In short, many pensioners and their families have already been reduced to poverty, and Greece’s creditors want pensions to be slashed further!

Now those reading this may feel compelled to ask: but what else can be done? The fact of the matter is that Greece is now in this mess, and has to play by the rules. Well fortunately there are many possible alternatives to austerity model (which, btw is in place because it serves the interests of financial oligarchs and not the public at large).

The alternate scenario that is most written about is Greece’s exit from European institutions. Whilst the coverage focuses of “Greece leaving the EU” -- the more likely scenario is that Greece may leave the 19-member Eurozone (European Monetary Union) but remain in the 28-nation European Union. Great Britain, for instance, is in the EU but not the Eurozone.

Another alternate scenario has been put forth by Greece’s new government: Greece could follow the example of Iceland and nationalise its banks, rather than bail them out with further IMF and bank loans that must be repaid by further cutting of pensions, schools, health care and social services.

Others too have put forth an alternative scenario. Economists who have realized that the austerity model doesn’t work. See this blog: “MODEST PROPOSAL” that says: “The establishment of this blog coincided with our campaign for a rational resolution of the euro crisis. By we, I mean Stuart Holland and myself. Such a resolution, we felt, was always feasible within the current institutional framework but requires clear vision and political will to implement. Moreover, it can be agreed to by people of different political persuasions since it is founded upon a minimalist, common sense, set of assumptions and policy recommendations.”

Economists such as Joseph Stiglitz, Thomas Piketty, Marcus Miller and others have also put forth alternative scenarios. “Austerity drastically reduces revenue from tax reform,” they write “and restricts the space for change to make administration accountable and socially efficient.”

An excerpt from the letter published by the economists read as follows: “Consider, on the other hand, a rapid move to a positive programme for recovery in Greece (and in the EU as a whole), using the massive financial strength of the Eurozone to promote investment, rescuing young Europeans from mass unemployment with measures that would increase employment today and growth in the future. This could both transform the economic performance of the EU and make it once more a source of pride for European citizens.”