- >>

- INDIA

Contrary to what Prime Minister, Narendra Modi announced at Houston’s NRG Stadium, all is not well in India. In the past few months, protests have seeped through states like wildfire. Students have been victims of institutional violence. Discourse on nationalism has polarized the nation. In the midst of the socio-political noise lies the economic cacophony.

The expectation for FY20 encompasses a GDP growth rate of 5%, which is the lowest witnessed by our country in 11 years. Private consumption is expected to grow at a 7 years low of 5.8%. While the expected growth rate in agriculture is 2.8% (not surprisingly, lowest in 4 years), it is the performance of the manufacturing sector that is worth noting.

Given the thrust towards making in India, it is baffling that the expected growth in manufacturing is approximated at 2% - lowest in 15 years. The envisaged 1% growth in investment is also the slowest rate witnessed in 17 years. Our telecom industry has consolidated to a loss making market of 4 players, with Vodafone Group contemplating an exit from India all together if the struggle continues. Let’s not forget that back in 2016, Vodafone had pumped INR 47,000 Crores ($7 Billion) into its Indian entity, becoming the largest foreign direct investment in India till date. That our policies and regulations have carved an exit path for the largest FDI may serve as a red flag for future foreign investments.

The premature secondary exits of venture capitalists from assumedly rocket start-ups cannot be ignored. Investors like Norwest, SAIF, Bessemer and Accel cashed out of Swiggy while Sequoia Capital, Times Internet and the Chan Zuckerberg initiative (Mark Zuckerberg’s impact fund) cashed out of Byju's– signalling some form of distress.

To top it all, inflation has risen from 1.97% in January 2019 to a 7.35% in December 2019 – well above RBI’s comfort level. It is evidently an understatement to say the economy is in distress relative to the past few years.

Against this backdrop, it is no wonder that all eyes were on the Finance Minister’s announcement of the Union Budget 2020-21 on Saturday. The expectations were high. The poor performance of all the aforementioned economic indicators put forth a bleak picture for our Finance Ministry, given the limited space to maneuver. A strong monetary stance would have further impacted inflation. A strong fiscal policy of tax deduction would have embedded the fiscal slippage, given that the fall in nominal GDP growth alone amounts to a 11 bps slip in the fiscal deficit ratio.

What was undisputed however is that the Government will need to create more confidence in the economy. It was equally imperative for the government to understand that it is difficult to make in India with an unhealthy, uneducated and impoverished population – and ergo, budget allocations on social and development domains of health, education and welfare must not be ignored.

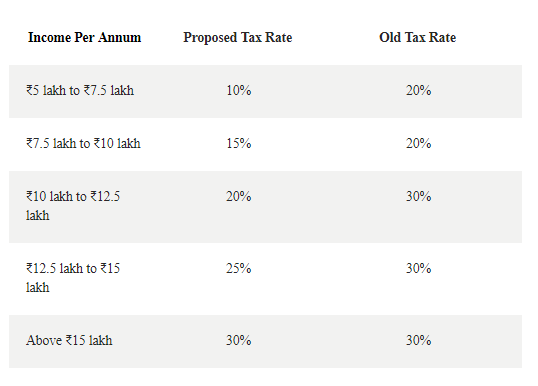

Nirmala Sitharaman’s Budget pillared in three themes and chose a fiscal path, with the announcement of a new tax regime. In this, income tax slabs are lowered for those who forgo exemption. The Budget also gave its taxpayers the choice to avail exemptions by continuing to pay at the old rates. However, the Finance Minister also announced that she has reduced exemptions of different nature from 100 to 30.

The proposed tax deduction is progressive, with the tax savings being most for those in the lower income bracket. Taxpayers with high income of ₹15 lakhs plus will see no deduction benefits from the budget.

Additionally, the Budget also signalled an increase in government spending with the aim to create jobs. This is particularly evident in the infrastructure segment. The Budget has proposed provision of ₹1.7 lakh crore for transport infrastructure and ₹18,600 crores for a Bengaluru suburban rail project. Chennai-Bengaluru expressway, electrification of 27,000km of lines, building of solar power capacity for Indian railway are in the proposed pipeline. Additionally, the government will monetise 12 lots of national highways and develop 100 more airports by 2024. Sitharaman stressed on skilling the youth so that they participate in these infrastructural developments via the axiomatic newly created jobs.

It is understandable as to why Sitharaman chose a fiscal route - the aim, as per her speech, was to boost income and enhance purchasing power. It is however, equally imperative to note that this might lead to notable reduction in the government’s revenue. India’s direct tax collections has grown merely by 2.7% so far in FY 2019-20 against the budgeted target of 18.6%. One can only hope that the ministry has indeed budgeted its tax collection - accounting for the proposed deductions - more realistically for 2020-21 so as to make this budget a realistic plan, as opposed to verbal promises.

In terms of the undisputed expectations from the budget, it is too early to comment on whether this Budget will increase confidence. Theoretically, it should with the expansionary fiscal policy. One can however, surely comment on the Budget’s inclination (or lack thereof) towards social indicators.

Comparison with the previous year’s budget allocation highlights that the current allocation is not much of an improvement. While health allocation increased by 6.9% relative to the previous year, education allocation increase is a mere 4.7%. Allocation for Scheduled Castes and Other Backward Classes has witnessed a 4.5% increase. The corresponding figure for Scheduled Tribes is 1.5%.

It should be noted that the allocation for each of these areas for FY 2019-20 was merely between 1.5 to 3.5% of the total proposed expenditure for the year (which was ₹27,86,349 Crores). It’s reasonable to extrapolate that the allocation for FY 2020-21 is approximately within the same bracket. The Union Budget therefore, yet again fails to recognise the importance of social and human resource development despite its transcript imbibing the words ‘economic development and caring society.’

Overall, with its thrust toward fiscal expansion, the budget may provide the confidence to boost consumption, reducing some distress. However, with its below par allocation for social and development domains, the Budget does not do justice to its three theme. Given that funds are after all limited, it appears that the government’s concentration is on short term relief from distress.

Dr Jaskiran Bedi is an economist, development advisor and author.